Bitcoin Energy Consumption

VeradiVerdict - Issue #136

On May 31, 1999, as the dot-com economy was beginning to take off, a Forbes article was published that claimed that it was “reasonable to project that half of the electric grid will be powering the digital-Internet economy within the next decade.” The piece accused the internet—and, specifically, hardware companies—of “burning up an awful lot of fossil fuels” and setting the world on a dangerous trajectory of energy usage.

Source: Forbes

When the California energy crisis hit in 2000, resulting in a nationwide conversation about energy usage, this narrative entered the mainstream. Dozens of other high-profile publications cited the Mills report, claiming that the internet was on track to gobble up the national energy supply. Internal reports by JP Morgan, Bank of America, and Deutsche Bank also cited these figures “with little or no indication that there was even a debate about them.” For such a provocative claim, there was a shocking degree of consensus.

The problem? The projections were wrong. Mills’s calculations were fraught with errors, resulting in a figure for internet power usage that, according to subsequent estimates, was at least a factor of eight too high. The data today, two decades after the Forbes article, clearly illustrates that these doom-and-gloom projections were way off-base. Even the most aggressive projections today show the internet only consuming 20% of electricity by 2025, and many tech giants are fully transitioning to renewable energy.

In other words, even though early energy projections for the internet relied on outrageous assumptions and output highly inaccurate results, the narrative caught on.

The debate—if it even qualifies as one, given how one-sided it can sometimes feel—surrounding Bitcoin’s energy usage today bears a striking resemblance, in my view, to these criticisms of the early internet. While eye-catching headlines, including Tesla’s recent proclamation, are quick to paint cryptocurrencies as accelerators of climate change, the issue is deep, nuanced, and filled with misconceptions.

Paving the path for a sustainable future is a topic of existential importance. As a result, any accusation of a government, corporation, or technology jeopardizing our ability to overcome climate change should be taken extremely seriously. But they should not be used lightly. Being wrong, like we were in the early 2000s, has consequences: it distracts attention from the real obstacles to long-term sustainability and delays progress to overcoming them.

This post is not meant to be comprehensive, nor is it intended to be the “last word” on the topic. However, this post outlines my framework for thinking about the issue of Bitcoin’s energy consumption as both a supporter of the cryptocurrency and someone who cares deeply about the issue of climate change.

Bitcoin uses energy for a reason.

While digital currencies had existed before Bitcoin, they ran into a number of technological problems that forced them to remain centralized, limiting their potential. Most notably, Satoshi Nakamoto solved the difficult double-spending problem in which past digital abstractions of value could simply be infinitely replicated, such as copy-and-pasting an image. Bitcoin, in short, was the first decentralized digital currency to truly be scarce.

For this blockchain to remain secure, a “consensus algorithm” is needed to validate transactions. Satoshi, in designing the system, could have simply instituted a majority-vote algorithm. In other words, each node has a single vote and if a simple majority (>50%) of network participants affirm the validity of a transaction, it is confirmed. The issue with this, though, is that a malicious actor could create an infinite number of these nodes, overpowering the “honest” nodes; since there is no cost to creating an additional node, there is an incentive to create fake, or “Sybil,” identities. This is called a Sybil attack.

Satoshi’s great insight was that a blockchain could be resistant to Sybil attacks if there was a cost to running a node. Inspired by this idea, Bitcoin uses a consensus algorithm called “proof-of-work.” Bitcoin miners, the nodes that validate transactions, are forced to solve computationally difficult mathematical puzzles, oftentimes with specialized pieces of hardware. Since this process consumes energy, which has a non-trivial cost, the Bitcoin blockchain makes it extremely difficult for an attacker to overwhelm the network.

Importantly, this energy is not “wasted,” as it is sometimes described in the popular media. Once you understand the rationale for why proof-of-work was chosen, it becomes clear that Bitcoin’s energy consumption is a feature, not a bug of the system.

While proof-of-work is used by Bitcoin, Litecoin, Monero, and other prominent cryptocurrencies, new, less energy-intensive consensus algorithms are being deployed. Ethereum, for example, is currently transitioning to proof-of-stake, a validation process that doesn’t require the same levels of energy consumption. For that reason, the energy debate is way more narrow than many think. It’s not an argument against cryptocurrency or decentralization broadly, as it is sometimes framed. It is really a criticism of a specific type of consensus process: proof-of-work.

Quantifying Bitcoin’s emissions.

Measuring Bitcoin’s energy usage is relatively simple: you can simply look at publicly-available hash power, network difficulty, and mining rig efficiency statistics to arrive at a high-conviction estimate.

However, energy consumption and carbon emissions are two very different things. While they may be correlated, emissions are determined by the type of energy used, not the quantity. Since we’re missing important information about Bitcoin miners, such as the hardware they use and their energy sources, making claims about emissions with any confidence is extremely difficult.

Despite this challenge, a number of academics have attempted to quantify Bitcoin’s carbon footprint. The most widely-cited paper on the topic, published by Camilo Mora and other faculty at the University of Hawaii, arrives at a harrowing prediction:

Here we show that projected Bitcoin usage, should it follow the rate of adoption of other broadly adopted technologies, could alone produce enough CO2 emissions to push warming above 2°C within less than three decades.

Despite being among the most hyperbolic projections, the Mora paper is arguably the most influential piece of research related to the proof-of-work debate. Media coverage of Bitcoin’s energy usage, when investigated closely, can usually be traced back to the Mora paper’s numbers. And the report’s dramatic title—“Bitcoin emissions alone could push global warming above 2°C”—has become an ingrained assumption, however fallacious, that many people hold. Given the Mora paper’s importance, it is worth diving into it further.

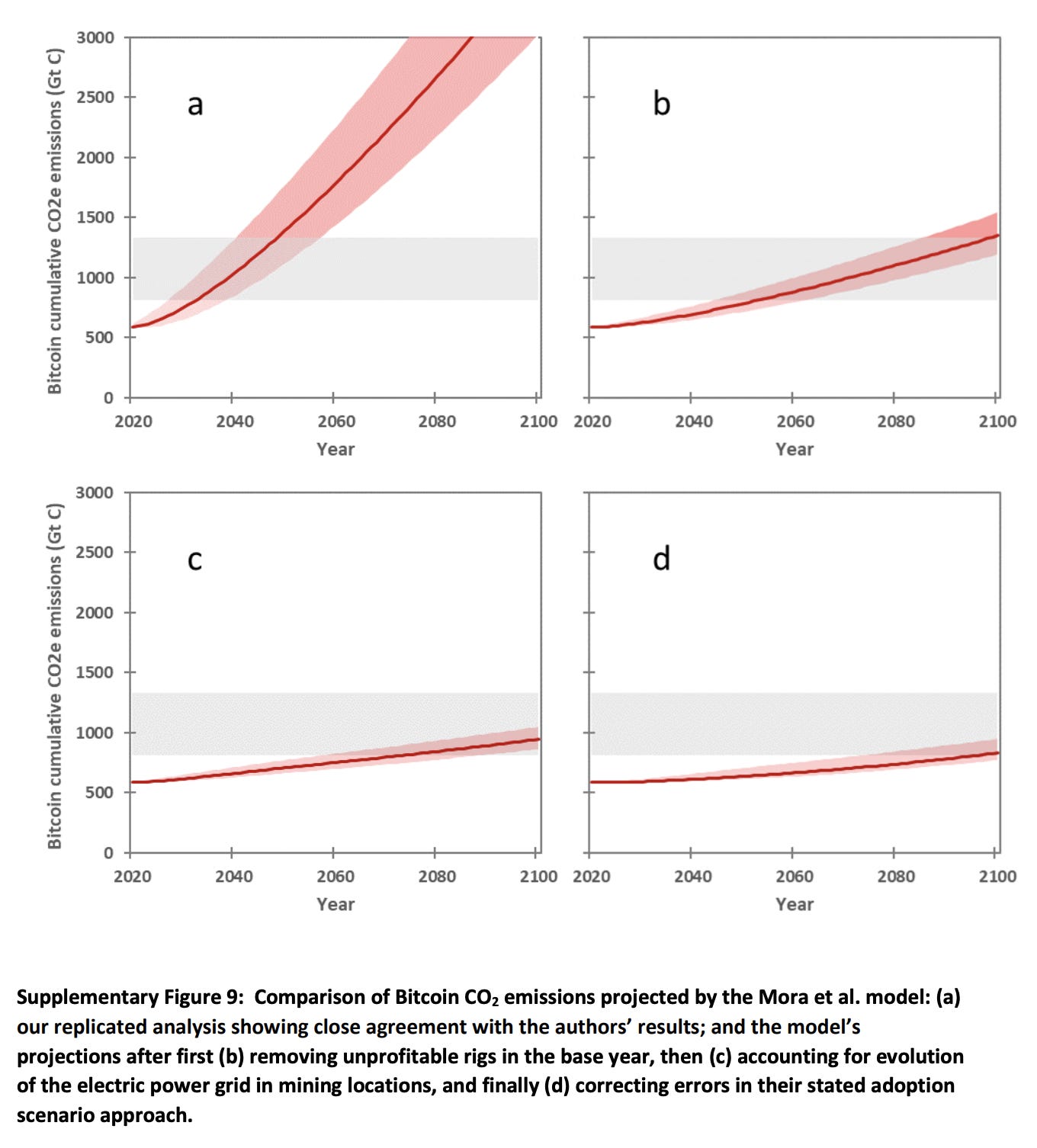

The report’s methodology is relatively straightforward. They estimated the efficiencies of mining rigs, used the average carbon emissions of their relative locations, and incorporated a projection of Bitcoin’s growth to measure future emissions.

However, several recent papers have directly disputed Mora’s findings, pointing out a series of mistakes that resulted in a drastic overestimation of Bitcoin’s emissions. I’ll quickly summarize these objections.

Doesn’t account for energy-related technological improvements. The study holds both mining rig efficiencies and grid carbon intensities constant over the next century. In other words, it assumes that mining hardware and energy grid emissions will remain unchanged over the next 100 years. This is a pretty unbelievable assumption. In the words of one critic: “This dubious choice ignores the dynamic natures of mining rig and power grid technologies and violates the widely-followed practice of accounting for technological change in forward-looking energy technology scenarios.”

Predicts an unprecedented speed of Bitcoin adoption. Mora, et al. use the growth trajectories of 40 past technologies (such as cell phones, computers, and vacuums) to predict Bitcoin’s growth. While this approach seems sensible, it arrives at some extremely unreasonable adoption predictions:

Specifically, Mora et al. assume that Bitcoin transactions— which totaled 104 million in 2017, representing a mere 0.03% of global cashless transactions—would abruptly leap to 78 billion by 2019 in the fast scenario (a 750x increase in only 2 years), to 11 billion by 2020 in the median scenario (a 108x increase), and to 8 billion by 2023 in the slow scenario (a 76x increase). All three adoption scenarios follow steep logarithmic growth trajectories thereafter, which are conspicuously inconsistent with historical trends (Supplementary Fig 4), and which mathematically can only lead to large near-term emissions increases.

By assuming a growth rate like this, the researchers guaranteed a high-emission estimate. If, instead, Bitcoin had been compared with the velocity of other stores-of-value, which is relatively low, it would have resulted in a more reasonable projection.

Conflates transactions with energy consumption. After predicting Bitcoin transaction volumes in the future, the Mora study simply multiplies the number of future transactions by the current emission estimate for a “total emissions” value. This is mistaken at the core: energy consumption is based on block difficulty, not the number of transactions. In fact, miners’ energy consumption has remained relatively flat over the past three years (since Mora’s study) even while transaction volumes have reached new peaks. Even if Mora’s transaction projections are correct, there is no evidence to support that it would result in a proportional increase in energy consumption. In fact, most experts believe that Bitcoin’s energy consumption will decrease as time progresses due to the lower quantity of minted coins.

Source: Digiconomist

After considering these failures of the Mora study, Masanet, et al. don’t pull any punches with their conclusion:

The results show that, had the authors avoided the key errors we described above, their own study design would have yielded much different, and far less alarming, projections of future Bitcoin carbon emissions. That said, we find the study design itself sufficiently flawed—e.g., use of transactions as driver, comparisons to 40 unrelated technologies, ignoring rig evolution—that such corrections alone are not enough to salvage the authors’ approach. On these bases, we argue that the Mora et al. scenarios are fundamentally flawed and should not be taken seriously by researchers, policymakers, or the public.

When Mora’s study is replicated without falling prey to these errors, the emission projections are far more tame. Just compare Mora’s original predictions (graph A) with those after correcting the study’s fallacious assumptions (graph D). The difference is night and day: emissions look relatively flat over the next several decades, hardly a cause for panic.

Source: Masanet, et al. 2019

This section has been a little in the weeds, but here’s the take-away: quantifying Bitcoin’s emissions is a difficult problem and many of the most alarming projections rely on deeply flawed methods. While we’ve specifically picked on the Mora study, in large part because of its sensationalism in the news, similar mistakes are commonly made by other researchers.

There’s no doubt that understanding Bitcoin’s carbon footprint is important. It is equally important, though, to identify, scrutinize, and correct inflammatory predictions that contribute little of merit to the conversation. The next time you see a new statistic related to Bitcoin’s energy consumption, it’s worth tracking down the original study. Chances are, you’ll find something that surprises you.

Comparing apples to apples: the energy consumption of comparable technologies.

Two elements, in particular, of the discourse surrounding Bitcoin’s energy consumption frustrate me. First, it seems to be an arbitrary and selectively-applied standard. We’ve rarely, if ever, used energy consumption to make a value judgment on other technologies, so why start with Bitcoin? Relatedly, the lack of comparisons that are made surprises me. Yes, Bitcoin consumes energy. That much is obvious. The more important question, in my view, is how it compares to other technologies, particularly the ones that it could be credibly viewed as an alternative to.

According to the Cambridge Center for Alternative Finance, Bitcoin currently uses around 110 Terawatt Hours per year of energy, accounting for 0.55% of global electricity consumption.

While estimates for energy consumption, as we’ve learned from the Mora study, can be inaccurate, I’ve tried to compile some reasonable estimates for other related technologies. I’ve personally found it helpful for contextualizing where Bitcoin falls in the grand scheme of things.

The most obvious comparison is Centralized Finance (CeFi), which is no stranger to energy consumption. Physical bank branches, back-end servers, and ATMs alone account for a total of 100 TwH a year, which is comparable to Bitcoin. And that’s excluding other high-emission practices of the banking sector, from long-haul trucking to corporate private jet flights.

Since Bitcoin is billed as “digital gold,” it also deserves to be compared to the physical mining of earth metals. By one estimate, mining $1 of aluminum consumes nearly ten times as much energy as mining $1 of Bitcoin. However, Bitcoin currently consumes more energy than gold and copper on a dollar-for-dollar basis. As Bitcoin’s mining pool transitions to renewable energy, a change that is much more difficult for the location-dependent metal mining industry, Bitcoin will likely become more “green” than gold.

Other comparisons illustrate the absurdity of the alarmism surrounding Bitcoin. The worldwide consumption of YouTube videos consumes around 600 TWh a year, six times that of Bitcoin. Video gameplay alone consumes 104.7 TWh per year, roughly the same as Bitcoin, and from far less renewable sources. Clothes dryers in the US consume 93.6 TWh per year, and that’s just a single country. The annual energy used by idle home devices, or electronics that are plugged in but inactive, in the US alone could power the Bitcoin network for 1.5 years.

I could go on with the comparisons, but I think I’ve made my point: everything uses energy, oftentimes more than you’d expect. As a result, energy consumption is not intrinsically bad, nor is it a particularly useful framework for judging the moral worth of a technology or activity.

Bitcoin’s relationship with renewables.

While discussing the quantity of energy consumption is useful, a TWh statistic misses the type of energy that is consumed, which is essential for measuring Bitcoin’s carbon footprint.

What makes Bitcoin mining unique is that it is truly location-agnostic. Miners, in fact, are financially incentivized to find inexpensive electricity sources, regardless of where they may be. As a result, Bitcoin mining naturally gravitates towards renewable energy; it is cheaper, has irregular patterns that can be arbitraged, and oftentimes has surpluses. Estimating the proportion of renewable energy powering Bitcoin is difficult, but one report claims 73% of the mining pool is carbon-neutral, while another suggests a figure closer to 39%. Either way, it is still an above-average proportion of renewables when compared with the composition of other technologies, countries, and organizations.

To visualize the type of energy that Bitcoin consumes, let’s take a look at two locations with high concentrations of miners. Sichuan, the second-largest mining province in China, has a massive overbuild of hydroelectric power from a government project, nearly double the amount the power grid can support. Washington, to take another example, has one of the highest concentrations of miners in the United States due to the cheap hydropower from the Columbia River. Normally, this “curtailment” would go unused since electricity is notoriously difficult to transport over distances longer than 100 miles. Bitcoin mining, however, offers a simple way to monetize this excess clean energy.

Globally, curtailment is a big problem. In 2017, China curtailed 7.3TWh of solar power and the UK curtailed 1.49TWh of wind power. In California alone, more than 346GWh of solar and wind was curtailed in 2018, and it’s only expected to rise in the future. While renewable energy is now less expensive than many other sources, this issue of curtailment has discouraged the build-out of new clean energy projects. Finding an efficient way to minimize curtailment could be the key to a carbon-neutral future.

Bitcoin mining could play a big role in solving this problem by serving as an “energy buyer of last resort.” Curtailed renewable energy and energy sources far away from population centers now have a guaranteed and revenue-generating use: securing the Bitcoin network. Square and ARK Invest recently released a must-read report on this topic, entitled “Bitcoin is Key to an Abundant, Clean Energy Future.” While some criticize the model’s specific projections, the long-term vision is extremely compelling:

Our model demonstrates that integrated bitcoin mining could transfigure intermittent power resources into baseload-capable generation stations. It suggests that the addition of Bitcoin mining into power developers’ toolboxes should increase the overall addressable market for renewable and intermittent power sources. All else equal, with bitcoin mining, renewable energy could provision a large percentage of any locality’s power economically. As a follow-on effect, cost declines associated with scaling renewables should most likely accelerate, leaving them even more economically competitive at equilibrium.

Ross Stevens, founder of the financial institution NYDIG, articulates a similar point of view:

Since fossil fuels are already too expensive for Bitcoin mining, I think, confidently, the only long-term profitable Bitcoin mining will be powered by clean energy. [...] From my perspective, beyond the revolution in monetary policy that Bitcoin already represents, Bitcoin also represents the biggest catalyst the world has ever known for the development of abundant, clean, cheap energy.

In summary, Bitcoin mining as an “energy buyer of last resort” could have dramatic implications for the future of energy, making it cleaner, more reliable, and less expensive. It will take time, but there is, in my view, a reasonably high chance that we look back upon Bitcoin as a part of the solution to climate change, not a part of the problem.

Source: ARK Invest

The real question: is Bitcoin worth it?

By this point, we’ve covered a lot of ground. We’ve analyzed estimates for Bitcoin’s energy consumption, compared that with other technologies, and investigated the potential for Bitcoin to spur a transition to renewables.

While the original topic—is Bitcoin’s energy consumption a problem?—is disguised as a scientific question, it’s really a moral one. Nic Carter hits the nail on the head in his recent Harvard Business Review article:

But how much energy should a monetary system consume? How you answer that likely depends on how you feel about Bitcoin. If you believe that Bitcoin offers no utility beyond serving as a ponzi scheme or a device for money laundering, then it would only be logical to conclude that consuming any amount of energy is wasteful. If you are one of the tens of millions of individuals worldwide using it as a tool to escape monetary repression, inflation, or capital controls, you most likely think that the energy is extremely well spent. Whether you feel Bitcoin has a valid claim on society’s resources boils down to how much value you think Bitcoin creates for society.

Every technology, idea, or institution has tradeoffs. Your stance on Bitcoin’s climate footprint, then, isn’t really determined by Bitcoin’s energy consumption. More likely, it’s a reflection of whether you think Bitcoin is a net positive contribution to society. And changing people’s minds about that, from my experience, is far more difficult. It’s certainly possible, but difficult.

Being a climate-conscious Bitcoin owner.

As retail and institutional investors increasingly incorporate Environmental, Social, and Corporate Governance (ESG) considerations into their investment theses, I’ve had multiple people ask me about the moral consequences of buying Bitcoin. My personal perspective on Bitcoin’s energy consumption, to summarize the preceding sections, is as follows:

It is undeniable that Bitcoin consumes a large amount of energy, which, in the short-term, will add some carbon to the atmosphere. However, it will leave far smaller of a footprint than most estimates assume.

Energy is not “wasted,” it is used to power the most secure blockchain on Earth, allowing for second- and third-layer innovations that expand financial access for billions of people. This is enough of a social good, in my opinion, to justify an expenditure of energy.

The debate around energy quantity is not particularly useful; instead, we should focus on energy types. Bitcoin already uses large amounts of renewable energy and, as the “energy buyer of last resort,” could help propel us to a carbon-neutral future.

Even if you disagree, one way to dodge the energy consumption debate entirely is just to purchase carbon offsets; that way, you can ensure your purchase of Bitcoin is carbon-neutral (or even negative). As we’ve seen, calculating a precise amount of carbon emitted from your personal engagement with Bitcoin is difficult—it’s not as simple as dividing hashpower by the number of transactions—but some good faith contribution (e.g., 10% of the value of your BTC holdings) can go a long way. Ninepoint, a Canada-based Bitcoin ETF, announced this month that they were purchasing offsets for their holdings. If you’re interested, I’d suggest using Nori, but there are other simple ways to purchase small carbon offsets.

On a final note, I hope to shift the discussion slightly. Instead of judging the uses of energy, which is a strict and selectively-applied standard, let’s focus on making energy production as clean as possible. Purchase offsets. Support renewable energy projects. Vote for a carbon tax. The list goes on. But don’t make Bitcoin the enemy: it only distracts us from completing the difficult work of creating a sustainable future.

- Paul V

LETS MEET UP

Bitcoin 2021, Miami, June 3-6

Puerto Rico, June 7-9

ABOUT ME

Hi, I’m Paul Veradittakit, a Partner at Pantera Capital, one of the oldest and largest institutional investors focused on investing in blockchain companies and cryptocurrencies. I’ve been in the industry since 2014, and the firm invests in equity, early stage token projects, and liquid cryptocurrencies on exchanges. I focus on early-stage investments and share my thoughts on what’s going on in the industry in this weekly newsletter.