Synthetic Derivatives

VeradiVerdict - Issue #143

DeFi, in just over a year, has already begun to chip away at many of the legacy financial system’s core use cases. Some of the core building blocks of DeFi—such as lending protocols and decentralized spot exchanges—have already discovered product-market fit. But many of the most integral elements of traditional finance have yet to be disrupted.

Derivatives could be the next financial “lego block” to be disrupted by DeFi. To get an idea of how massive the opportunity is, spot trades (stocks, bonds, commodities, etc.) accounted for only 30% of total trading volume in 2019; futures and options drove the other 70%. Whichever way you slice it, the conclusion is clear: there’s a lot of demand for derivatives.

While derivatives for digital assets are still in their early days, we’ve already observed a similar trend. In December 2020, the average daily trading volume for crypto derivatives was over $1.3T, over half of the entire industry’s market capitalization. In addition, the trading volume of derivatives has officially overtaken spot volume, making up nearly 55% of the total.

Where are these derivatives traded today?

The vast majority of crypto derivatives are currently routed through centralized exchanges, such as Binance, OKEx, and others. This makes intuitive sense: centralized exchanges are able to amass large amounts of liquidity, offer reasonably competitive rates, and are effective at onboarding large financial institutions.

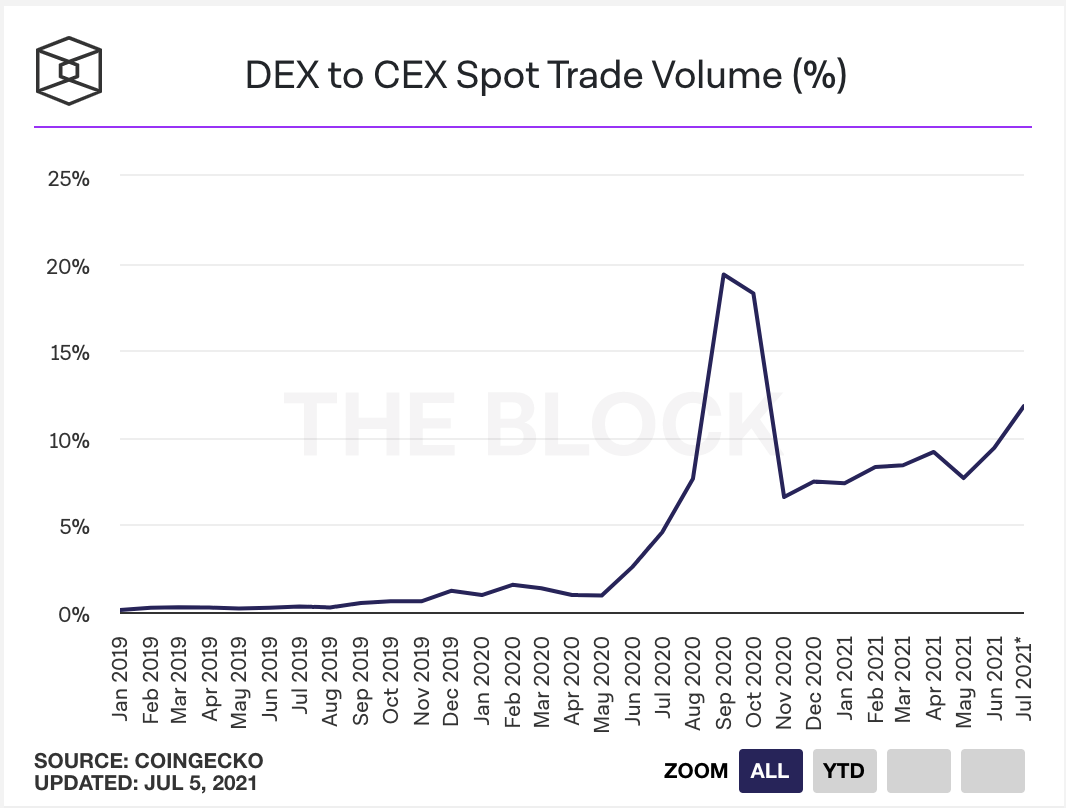

Source: The Block

A similar dynamic occurred in the early days of decentralized spot exchanges. The vast majority of cryptocurrencies were traded on centralized exchanges, such as Coinbase and Binance, due to their user-friendliness and low fees. Over time, DEXes, such as Uniswap or 0x, were able to offer value in ways that centralized exchanges simply could not: a wide offering of trading pairs, high liquidity, and so on. Today, nearly 15% of total spot trading volume is settled on decentralized exchanges, an incredible achievement for the ecosystem. And it’s just getting started.

Source: The Block

We believe that a similar narrative will unfold for derivatives.

Centralized exchanges have a number of limitations which have become apparent from the market’s recent volatility. These include:

Opaque, behind-the-scenes mechanisms which can be controversial in the event of forced liquidations.

Reliance on institutional trust, which prevents some speculators from purchasing long-term derivatives out of fear of the issuer’s insolvency.

High operational inefficiency which, among other things, slows the addition of new trading pairs.

Regulatory risk which may affect accessibility, such as Binance’s recent issues with the UK FCA.

As decentralized derivatives exchanges mature, we believe that they can deliver a superior product, as they have done in spot markets. The question, we believe, is not if this decentralization occurs, but when.

Introducing SynFutures, where you can trade anything, anytime.

SynFutures is a decentralized derivatives exchange tackling this huge opportunity. The company recently raised a $14M Series A which Pantera also participated in. The team also rolled out the Closed Alpha of their platform in June, targeting a mainnet launch later this month.

Put simply, SynFutures is the Uniswap for futures contracts: users can easily list their own futures contracts of arbitrary trading pairs with just a few clicks or purchase their desired derivative contract in a permissionless way. It is designed to be accessible to anyone, highly decentralized, and compatible with as many trading pairs as possible. The protocol is currently built on Ethereum and Polygon, a layer-2 scaling solution, to minimize transaction fees. To take a sneak peak at the Alpha version of the product, sign up here and check out this short tutorial.

Source: SynFutures

The elephant in the room when it comes to synthetic derivatives is, of course, Synthetix, a rival derivatives liquidity protocol. SynFutures, we believe, is well-equipped to out-compete Synthetix in a number of ways:

More extensive trading pairs. Synthetix uses a governance process to roll out new assets, which can sometimes take months—as has been the case for Dogecoin—to actually arrive on the protocol. SynFutures allows the user to choose any trading pair they’d like—so long as it has a Chainlink price oracle or a Uniswap pool—and immediately purchase it.

Zero slippage is net bad. Synthetix’s promise of “zero slippage” seems good at face value, but actually exposes users to unlimited downside risk. In addition, sharp fluctuations in SNX, the protocol’s native token, could result in unintended losses for speculators. SynFutures avoids these pitfalls entirely.

Capital efficiency. Synthetix has a 450% collateralization ratio, resulting in the under-utilization of assets. SynFutures, on the other hand, puts 100% of users’ capital to work and allows them to lever up their positions.

For a more robust comparison with Synthetix, be sure to read their full piece.

How does the automated market maker (AMM) work?

Something unique about SynFutures is their sAMM, a first-of-its-kind automated market maker for synthetic assets. Here’s a short description of how it works:

Our sAMM lets LPs supply one asset of a trading pair (such as a stablecoin), where the smart contract automatically synthesizes the other asset within the pool. As an example, if you choose to use a stablecoin (i.e. USDT) to deposit into an ETH/USDT pool, you can supply the entire amount in USDT instead of an equal amount of each token.

50% of the value of your deposit will stay in USDT, and the other 50% will be used as margin to represent a synthetic 1x long futures contract in ETH, giving you exposure to a derivative position.

When the long position is created, the sAMM will also enter into a short position of an equal amount for the user. The long and short positions counteract each other, so there’s no added risk when the user adds liquidity to the pool.

To summarize, a futures contract has two elements: a base and quote asset. Interestingly, an LP can choose to supply single-sided liquidity; in other words, they can choose to supply either (or both) of the assets in the trading pair. When they supply liquidity, the sAMM is, in essence, acting as a market participant with its own margin account. To keep these mechanics simple, though, you can think of liquidity provision as similar to being an LP for a typical AMM pool, just that you must also ensure that you meet the pool’s margin requirements.

SynFutures also has a unique liquidation mechanism. As opposed to Maker’s process of automatically liquidating under-collateralized accounts, SynFutures can force accounts that don’t meet margin requirements to reduce (and offset) their positions. This is a “happy medium” specifically for derivatives that minimizes systemic risk to the protocol while simplifying the liquidation process.

What’s on the roadmap?

SynFutures V1 will be launched on mainnet later this month, which will support fixed margin futures, leverage, and all Chainlink-supported assets and Uniswap pools.

Moving forward, a number of exciting new products will be rolled out:

Index futures, such as speculating on Bitcoin mining difficulty in the future.

Shared margin futures, including perpetual futures and decentralized futures basis trading.

Cross margin futures, enabling an “auto hedger” solution for impermanent loss.

Source: SynFutures

We believe that derivatives will be as big of a part of the DeFi ecosystem as it is for the legacy financial system. Protocols that are able to deliver a superior product to centralized alternatives, similar to Uniswap and spot trading, will seize this massive opportunity.

SynFutures may still be in their early days, but we believe that they’ve already created a differentiated product that is ready for the public. We’re thrilled to be along with them for the ride.

- Paul V

DIGESTS

Market Wrap: Ether Outperforms Bitcoin as Crypto Sentiment Improves

Ether is attempting to break above the 50-day moving average for the first time since March.

NEWS

CryptoKickers Is Bringing NFT Sneakers to the Hypebeasts of the Metaverse

Sole Selector lets users design and mint their own sneaker NFTs on the Solana blockchain.

Kraken Casts More Doubt on JPMorgan Call Over Grayscale Bitcoin Trust ‘Unlocks’

Kraken is disputing the premise that a wave of GBTC shares hitting the secondary market will drive the price of bitcoin lower.

REGULATIONS

Binance CEO ‘CZ’ Responds to Global Regulatory Pressure, Calling Compliance a ‘Journey’

"We are seeing wider adoption of cryptocurrencies globally and the need for clearer regulatory frameworks in different countries," said CZ.

IN THE TWEETS

NEW PRODUCTS AND HOT DEALS

Zerion Raises $8.2M to Make DeFi as Easy as Coinbase

The DeFi portal has processed over $600 million in transactions since the beginning of the year.

Mark Cuban-backed NFT platform Mintable raises $13 million in Series A

NFT platform Mintable, backed by billionaire investor Mark Cuban, has raised $13 million in Series A funding.

LETS MEET UP

Paris, July 20-22, Ethereum Community Conference 4

New York City, July 26-28

Los Angeles, July 29-30

Mexico City, Aug 30-Sept 1

Coffee meetings or walks in San Francisco

ABOUT ME

Hi, I’m Paul Veradittakit, a Partner at Pantera Capital, one of the oldest and largest institutional investors focused on investing in blockchain companies and cryptocurrencies. I’ve been in the industry since 2014, and the firm invests in equity, early stage token projects, and liquid cryptocurrencies on exchanges. I focus on early-stage investments and share my thoughts on what’s going on in the industry in this weekly newsletter.