The State of Crypto Venture Capital in 2025

VeradiVerdict - Issue #337

Summary

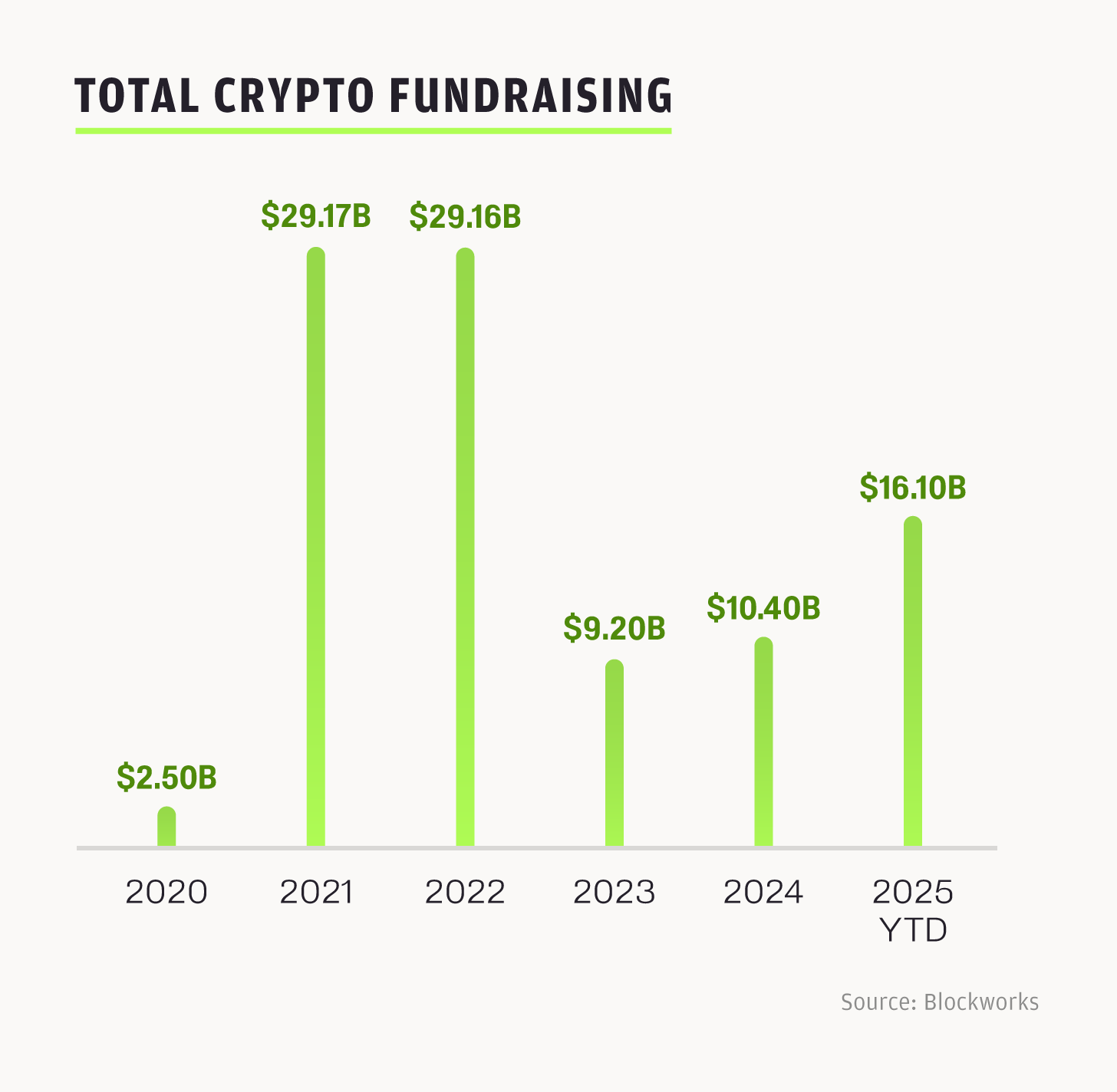

Year to date crypto companies have raised more than $16 billion with over 100 M&A deals, putting the industry on track to set a new record and already surpassing the total deal value of 2024.

This cycle is fundamentally stronger, driven by greater regulatory clarity in the U.S. and growing momentum globally.

The wave of strategic M&As and IPOs are set to carry forward into the next cycle.

Record-breaking M&A and IPO activity is reshaping and elevating the crypto landscape in 2025. This is fueling an influx of new capital, institutional interest, builders, and users to drive blockchain innovation and adoption. This is a pattern seen in other major technological shifts, where a multi-decade build-out precedes explosive growth. While AI's rise was sustained by decades of infrastructure investment, crypto is on a much faster path to maturity. It has the benefit of building on a more advanced tech stack, allowing it to compound progress with better tools, which is why the market's underlying momentum is now fundamentally different from previous cycles, driven less by speculative hype and more by strategic consolidation.

Momentum Is Accelerating: Why This Cycle Is Different

The crypto market has traced a sine-like pattern, having its ups and downs. Despite the slowdown in the venture capital space, activity under the surface has been bullish consequently due to regulatory tailwinds, a crypto-friendly administration, strong deal flow, companies like Robinhood doubling down in crypto and crypto’s deepening intersections with adjacent verticals. Since its peak in 2022, capital deployment crashed in 2023, recovery kicked in during 2024, and 2025 is seeing a marked acceleration. Q2 2025 alone saw 31 deals exceeding $50 million, with late-stage financing such as IPOs, mergers, and debt driving growth. Year to date, the crypto market has seen more capital enter the space ($16.1B), however crypto venture capital (VC) is mirroring traditional VC, as the capital is concentrated among a smaller number of funds. When capital concentrates, you typically get bigger checks but fewer deals overall. This is a reflection of many crypto companies maturing towards growth stage companies and it also points to the fact that the fundraising landscape has gotten more competitive than ever before for both founders and investors.

A conglomerate of forces is setting this cycle apart from the others. Token prices are rebounding, new products are launching, founders have more confidence to dive into the industry, regulatory tailwinds have provided clarity for stablecoins and digital assets, all unlocking capital into the space. Regulatory ambiguity has created friction between innovators and the Web3 space for years due to the fear of potential retribution. With the Trump Administration’s crypto-friendly attitudes, we have witnessed the cornerstone of on-chain adoption emerge through legislation, with The Genius Act and The Clarity Act. While we cannot say for certain how the deep future will be affected due to these bills, it is certain that these discussions and movements will shave off some hesitation towards investing in the space both intellectually and monetarily. Additionally, The Federal Reserve’s anticipated rate cuts in November are expected to drive more capital into risk assets, with digital asset trading systems (DATS) locking up capital in longer-tail assets. Investors are becoming less risk averse, creating a more enthusiastic flow of capital.

Investment allocation shifts with one-third of capital flowing into “bottom-up” opportunities like perpetuals, token launchpads, prediction markets, and novel DeFi primitives. The remaining two-thirds is targeting “top-down” plays, including DATS, real-world asset tokenization (RWAs), exchange-traded funds (ETFs), and companies entering public markets. These public market assets have dominated this cycle, which in turn allows the broader public better access to crypto assets, marking a very healthy sign for the industry.This balance illustrates a maturing market prioritizing both innovation and integration with traditional finance.

There is a short window where the blueprint of crypto legislation needs to take place, and with the current administration being pro-crypto, that window exists before the 2026 midterm elections. The DeFi Education Fund aims to protect software developers by submitting their response to the Senate Banking Committee’s Digital Asset Market Structure Request for Information and recently publishing a discussion draft of the Responsible Financial Innovation Act of 2025. Last week, the Wyoming Blockchain Symposium 2025 focused on digital asset regulation with an emphasis on the urgency of the U.S. establishing clear crypto regulations and the need for a balanced market structure. Members of the current administration attended the symposium, with an agenda to push forward-thinking regulation. Going into the first quarter of 2026 we can anticipate an even stronger foundation from a regulatory standpoint, one that we have never seen before in previous cycles especially with a ticking clock.

Token Listings and the IPO Market Re-opening

Token listings have declined in 2025, with fewer new tokens holding gains, creating a downstream drag on deal flow. Projects reliant on token launches are finding it harder to secure funding without market traction. In contrast, the IPO window has reopened with 95 companies listed on U.S. exchanges in 2025, raising $15.6 billion by mid-June, which is a 30% increase from 2024. Crypto-related IPOs, including Circle and BitGo, are leading the charge, creating a new trend where investors are allocating towards crypto stocks instead of tokens. Circle’s IPO on June 5, 2025, was a pivotal moment, pricing at $31 per share and rose to $233 by mid-July, delivering over 5x returns and a $44.98 billion market cap. As of recent, Figure and Bullish IPOed with Bullish being the first to raise $1.15 billion partly through stablecoins. BitGo’s planned IPO and $100 million raise in 2023 during a bear market emphasizes investor interest. Crypto companies are now optimizing for revenue and growth over speculative token launches.The surge in crypto IPO and other “top down” plays is attracting traditional investors through the lens of stable, revenue-driven business models over volatile cryptocurrencies. This is just the start of the IPO pipeline, with many more in line in the coming months.

Acquisitions and Industry Maturation

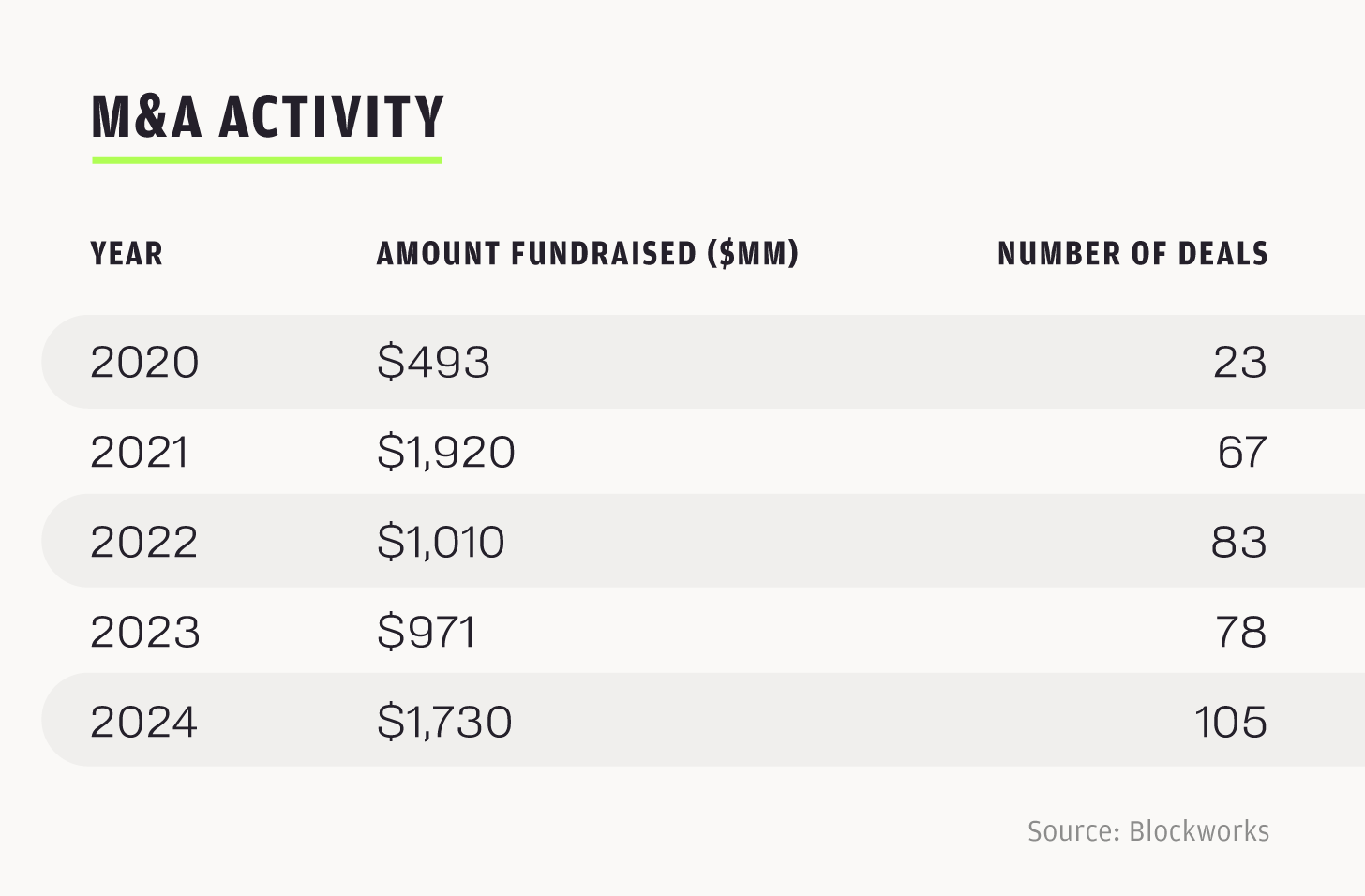

2024 was a record year for acquisitions with over 100 mergers and acquisitions (M&A) totaling $1.73 billion and 2025 is set to surpass 2024 in deal count. From January to July of this year it is already at 76 deals and $6.23 billion, which is 3.6× 2024’s full-year dollar volume and is on pace for 130 deals if the current run rate holds. The momentum in 2025 is less about unleashing pent‑up demand and more a sign of the industry’s natural maturation. Strategic acquisitions, like Robinhood’s purchase of Bitstamp, show established players building integrated platforms. Robinhood's multibillion-dollar bet on crypto’s future is lending even further credibility to the ecosystem, as their crypto revenue surged 98% year-over-year to $160 million in Q2 2025, with the overall company revenue up 45% to $989 million and profits at $386 million. As a backbone of retail-focused stock trading, Robinhood’s embrace of blockchain rails emphasizes the shift toward mainstream, regulated infrastructure. In the same vein, late-stage deals, such as Securitize’s $400 million raise from Mantle in Q2 2025 for RWA tokenization, and Kalshi’s $185 million raise at a $2 billion valuation for prediction markets, highlight a focus on revenue-driven, regulatory-compliant models.

These moves reflect crypto’s focus on building with financial incumbents, and not just chasing speculative opportunities.

The Macroscopic Intersection of Crypto

Crypto is no longer siloed as it’s converging with today’s cutting edge technology and global finance. In AI, OpenMind’s OM1 + FABRIC stack addresses the “missing layer” in the robotics industry, allowing different robots to work together through a decentralized approach. Worldcoin’s iris-scanning identity verification system leverages a blockchain-based identity layer that could enable AI agents to authenticate and transact autonomously, addressing the critical challenge of agents interacting securely in crypto. Decentralized AI platforms like Sahara AI ( a decentralized alternative to Scale AI) and Sentient (a decentralized Hugging Face) are disrupting traditional AI infrastructure. The application layer of crypto AI is still very nascent, but the potential that it harbors could create an entirely new market structure through on-chain agents and trading systems that enable high-frequency trading of tokenized stocks.

In payments, stablecoins, particularly Circle’s USDC has become integral to global payment systems with The GENIUS Act further accelerating USDC adoption. Circle reported a 58.6% revenue growth to $579 million in Q1 2025. Analysts project stable coin transaction volumes could reach $250 billion daily within three years, and potentially even surpass legacy payment systems like Visa within the next decade if the momentum of growth continues. Enterprises like PayPal and Visa are exploring stablecoin integration, blending stablecoins into mainstream payment rails. Robinhood's integration of Arbitrum has allowed Robinhood users to transact USDC natively on Arbitrum, making stablecoin transactions more accessible to retail users. With the Robinhood partnership just being the tip of the iceberg, Arbitrum plays a key role in scaling stablecoin adoption and exemplifies how Layer 2 solutions are bridging crypto with traditional finance.

This intersection of the most critical industries is pooling experts from AI, fintech, and consumer tech, blurring industry lines. Crypto’s role as a backbone for decentralized systems is positioning itself as a critical layer in the global tech stack.

Looking Forward

We anticipate a structurally stronger market cycle in Q4 2025 and Q1 2026. The confluence of unprecedented regulatory clarity, expected rate cuts, and a significant influx of capital from strategic M&A and IPOs is creating a robust foundation. This newfound momentum, driven by a focus on real-world utility, is setting the stage for a period of accelerated growth. Our strategy is to capitalize on this by making concentrated, high-conviction investments in Series A companies poised to define their categories.

Year to date, the U.S. IPO market has surged with 224 IPOs. In the first half of 2024, there were 94 IPOs compared to 165 in the first half of 2025, reflecting a 76% increase. There have been 185 crypto-related deals in the first half of 2025 alone, projecting to surpass 2024’s 248 acquisition deals. High-profile successes like Circle alongside other TradFi giants acquiring crypto companies, is marking the strength of the imminent cycles.

The intersection of crypto with AI, payments, and infrastructure, combined with regulatory tailwinds and strong investor appetite, will push us into an era of accelerated growth. With this, we will continue cementing crypto's role as a pillar of global finance and technology.

- Paul Veradittakit

Business

Crypto Fund Pantera Seeks to Raise Up to $1.25 Billion for Solana Deal

Pantera Capital is seeking to raise up to $1.25 billion to create "Solana Co.," a Nasdaq-listed treasury vehicle dedicated to accumulating and staking Solana (SOL) tokens.

Coinbase Expands International Offerings

Coinbase announced the launch of new trading pairs and expanded its international product suite, targeting growth in non-U.S. markets.

Rarible Acquires Flipp, Expands Product Team

Rarible, a leading NFT marketplace, announced the acquisition of Flipp, a mobile-based crypto trading app.

Regulation

DEF & 110+ Partners Submit Coalition Letter on Developer Protections in Market Structure

On August 1, 2025, DEF submitted their response to the Senate Banking Committee’s Digital Asset Market Structure Request for Information and recently published discussion draft of the Responsible Financial Innovation Act of 2025.

Illinois Enacts Stricter Crypto Consumer Protection Laws

Illinois Governor J.B. Pritzker signed two new laws: the Digital Assets and Consumer Protection Act and the Digital Asset Kiosk Act. These laws empower state regulators to oversee crypto exchanges and wallet providers, require anti-fraud measures, cap ATM fees, and limit daily transactions.

Federal Reserve Ends Special Crypto Oversight Program

The U.S. Federal Reserve announced it will sunset its Novel Activities Supervision Program for crypto and fintech, integrating oversight of digital asset activities into its standard regulatory processes by August 2025.

New Products and Hot Deals

Aptos Labs' Shelby Protocol

Aptos Labs, with Jump Crypto, introduced Shelby: a decentralized hot-storage protocol offering sub-second reads, high throughput, smart contract-based access control, and integrated monetization.

Bybit & Tether in Brazil

Bybit partnered with Tether to accelerate crypto adoption in Brazil, offering USD₮ bonuses for new users, event sponsorships, and a national “Learn to Earn” campaign.

CryptoPunks Catch Fire Again

NBA Top Shot NFTs launched in Japan via vending machines, and CryptoPunks saw a surge in trading volume, signaling renewed institutional interest

This Week at Pantera

Blockchain Letter

Pantera’s August discusses how Digital Asset Treasuries (DATs) offer a path to higher returns than holding spot or ETFs by compounding yield into more token ownership per share, where Pantera has already deployed $300M across them globally.

Pantera in Time's Top Venture Capital Firms List

To spotlight the names molding the business landscape, TIME and Statista ranked 350 VC firms at the forefront of catalyzing innovation, supporting emerging startups, and driving the next generation of economic growth.

Pantera Capital's DAT Fund and the Crypto-Stock Wave

The fund leverages token compounding, premium equity issuance, and Ethereum-based strategies to grow NAV per share while mitigating downside through crypto exposure.

ABOUT ME

Hi, I’m Paul Veradittakit, a Managing Partner at Pantera Capital, one of the oldest and largest institutional investors focused on investing in blockchain companies and cryptocurrencies. I’ve been in the industry since 2014, and the firm invests in equity, early-stage token projects, and liquid cryptocurrencies on exchanges. I focus on early-stage investments and share my thoughts on what’s going on in the industry in this weekly newsletter.

If you have any projects that need funding, feel free to DM me on twitter.

thanks

VCs trade more than they invest in new startups