VeradiVerdict - How To Make Money On Lending Crypto - Issue #37

Hi, I am Paul Veradittakit, a Partner at Pantera Capital, one of the oldest and largest institutional investors focused on investing into blockchain companies and cryptocurrencies. I focus on early investments and want to share my thoughts and what’s going on in the industry in this weekly newsletter.

View this issue on my Medium blog here.

If you aren’t subscribed already, you can click here to subscribe.

Editorials

TL;DR

Lending is one of the hottest spaces in cryptocurrency innovation right now, with tons of companies figuring out novel ways to adapt and mix up the infrastructure of traditional financial lending products for the blockchain space.

Some key factors to look at when analyzing lending companies are: product, market, rates/collateralization, decentralization, liquidity, funding & traction, and biggest value proposition. All these contribute to what differentiates a company from the rest, and why they might be successful in the long run.

Six example companies in the space right now are:

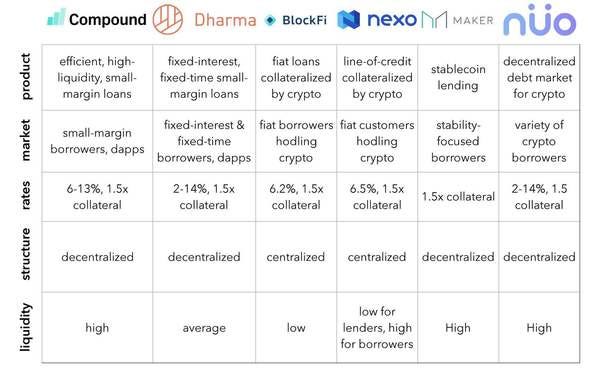

o Compound: efficient, high-liquidity small-margin loans

o Dharma: fixed-interest, fixed-time, highly secure small-margin loans

o BlockFi: fiat loans collateralized by users’ crypto

o Nexo: fiat line-of-credit collateralized by users’ crypto

o Maker: stablecoin crypto lending solution

o Nuo: decentralized debt market for lending/borrowing crypto

Regulations are one of the biggest considerations when looking at crypto lending innovation. Most of these companies run on smart contracts, which are regulated like the CFTC like any other financial contract.

Altogether, the market for lending is huge and has a lot of promising players for innovation.

Why lending?

With the traction and attention that cryptocurrencies have been getting recently, a lot of companies have started adopting traditional financial products, like lines-of-credit and loans, for the cryptocurrency market.

Much of these new cryptocurrency-centric financial products focus on lending––it’s one of the hottest markets for cryptocurrency innovation right now. Naturally, the popularity of the space invites a lot of companies to innovate and create products and tools here. Here’s an analysis of what I found to be six promising companies in the space, what they’re doing, and why I think they’re so interesting.

Categorically Analyzing the Companies

I focused on seven key factors to understand the ins-and-outs of the company, the kind of markets they were going after, and how they’ll be successful in the long-run.

1. Product. Essentially, what is it that they’re building, and why is it so important to the cryptocurrency lending market? Does it have value in other cryptocurrency spaces? How closely does it mimic the traditional financial products we’ve known of and in what critical ways does it differ?

2. Market. Who are the customers? Is it more focused towards first-time crypto users, or veterans of the space? Does it target Dapps and automated cryptocurrency loans or is it more human-user-oriented?

3. Rates & Collateralization. How secure are your loans (on both the borrower and lender side)? What benefits do you get, and what is the cost of capital?

4. Decentralization. Decentralization is a critical element to any blockchain technology––most traditional financial products use a centralized infrastructure to manage assets. Do these companies do the same? If not, how do they go about handling user assets and making loans?

5. Liquidity. As for any lending service, it’s important to know how easy it is to get your money back. Do decentralization or the blockchain protocol throw any wrenches in liquidity?

6. Funding & Traction. How’s the company doing overall?

7. Biggest Value Add. Put simply, after looking everything over, what one or two things define this company? What makes it stand out?

Looking through these seven key factors will give you a fairly good understanding of the basic service that these companies are trying to sell, and why they might be so promising.

Compound

Product: Compound is essentially an algorithmic protocol that facilitates peer-to-peer (P2P) lending on the Ethereum blockchain without taking too much custody in user funds. It basically takes in funds invested by lenders and loans them out to borrowers, balancing the finances algorithmically so that the funds are never centralized in one deposit, account or wallet. It also algorithmically sets interest rates based on supply and demand. Because of the P2P and algorithmic nature, it mainly targets small margin loans, but offers fairly high efficiency. It also has a fairly robust tech suite and API to automatically interface with the protocol. Compound’s main vehicle for profits is by taking a small margin on the money it makes from loans and through its API suite.

Market: As mentioned earlier, the protocol mainly supports small margin loans, so one of the biggest applications in decentralized applications, or Dapps. Dapps that need to loan/borrow on a very rapid basis at high liquidity can easily interface with Compound’s API to get their business done seamless and securely.

Rates & Collateralization: Compound offers 6-13% interest back to lenders depending on the currency, which is pretty high for a decentralized lending protocol. All loans are collateralized to 1.5x the loan value, which helps add an element of security that might reinstate some of the investor confidence that decentralization can often erode.

Decentralization: Compound’s one of the most decentralized lending platforms out there, because of the algorithmic way they balance inbound investments from lenders and outbound loans to borrowers. It’s impossible to be 100% decentralized, and they need to cover the differences between lending and borrowing somehow, so they have some stake in user assets and some cryptocurrency of their own that they insert into the platform, but it’s definitely one of the more decentralized lending solutions out there.

Liquidity: With its algorithmic balancing protocol, Compound also offers fairly high liquidity to both lenders and borrowers. On the borrower-side, it’s 100% liquid and one can get a loan instantaneously––one reason why it’s so popular for Dapps. On the lender side, it’s fairly easy to pull out your loan because the protocol is always moving around assets to help balance things out.

Traction and Funding: Compound has raised $8.2 million from big name investors, like Bain Capital Ventures, a16z, and Polychain. It also notably has backing from Coinbase. The platform has gotten significant traction, with just under $40M USD in asset value on the protocol as of May.

Biggest Value Add: Compound’s biggest value is that it’s a high-liquidity, fast-lending tool. This provides massive value for Dapps that need to do quick, small loans efficiently.

Dharma

Product: Dharma, like Compound, offers a P2P cryptocurrency lending solution that channels investments made by lenders to borrowers. Dharma differs in that it offers a fixed-interest, fixed-time format to borrowers which gives it a little more structure, stability, and robustness. It also has a fairly robust tech suite that supports a lot of Dapp integration, which is nice because it enables fast, trustable loans with its protocols. Dharma, like Compound, takes a small margin on the loans it gives out and also charges developers for its API suite, which enables its profits.

Market: Dharma is very geared towards offering fixed-interest, fixed-time loans to borrows and also powers small margin-lending. This naturally sets it up to be good for first time cryptocurrency users who want a very trustable, understandable loaning mechanism and also Dapp developers who need quick, secure small loans.

Rates & Collateralization: Dharma’s rates are fairly competitive, with 2-13% returns on the lender side, depending on the type of cryptocurrency that’s being invested. Dharma algorithmically sets rates based on the supply and demand of cryptocurrency moving through the protocol. Dharma also has a standard 1.5x collateralization on all outbound loans, which helps preserve some of the security in lending.

Decentralization: Dharma is an end-to-end non-custodial and smart contract-based platform.

Liquidity: The liquidity on Dharma is fairly high and consistent; they offer 90-day loans, which means lenders lose access to their assets for 90 days, but borrowers can get loans approved within one or two days with their approval process. In general, the liquidity is high for such a centralized, established protocol.

Traction & Funding: Dharma has raised over $7 million in funding from Coinbase Ventures, Polychain, Passport Capital, and YC. It has processed over $6.4 million in cryptocurrency loans on its platform since its inception in 2018.

Biggest Value Add: Dharma offers a very trustable, and secure fixed-rate and fixed-interest lending service that will appeal to Dapp developers and traditional lenders alike.

BlockFi

Product: Out of all of the companies on this list, BlockFi offers the most traditional lending product. Users can invest cryptocurrency into the platform as collateral, and then take out loans in fiat (up to a limit determined by the collateralized amount) to use for everyday financial transactions––like paying off a mortgage, buying a car, etc. It essentially aims to bridge the gap between the fiat and cryptocurrency lending space by providing fiat loans collateralized by the cryptocurrency users put onto the platform. BlockFi can also afford to take larger margins on the loans that it gives out, because the loans are larger in nature and can thus sustain more profit per-loan.

Market: BlockFi’s products are mainly geared towards consumers who want fiat loans and are probably hodling cryptocurrency without an immediate vehicle to spend it or invest it. It’s not super targeted towards Dapps or small loans, but rather the larger traditional loans you’d expect from traditional banks.

Rates and Collateralization: BlockFi offers 6.2% back on cryptocurrency that you invest, which is much higher than you’d get from any traditional savings account or traditional loan. It’s also collateralized up to 1.5x of the loan value, and all of its assets are backed by accredited, established institutions which gives security to your money.

Centralization: Because it follows the model of a very traditional financial lending product, it is very very centralized, as most traditional financial tools are. It takes custody in user assets and everything is backed and SEC-regulated.

Liquidity: Because the platform offers such large loans, the liquidity is fairly low compared to other crypto lending solutions. It takes a while to get loans approved as a borrower, and as an investor, there’s a bit of friction to inserting your money into the platform and pulling it out.

Traction & Funding: BlockFi is doing exceedingly well financially, and has raised from investors like ConsenSys, SoFi, Kenetic Capital, and Galaxy Digital Ventures. On the customer-side, it’s doing really great too––with $53 million in cryptocurrency and fiat processed on the platform as of April 2019.

Biggest Value Add: BlockFi provides a really incredible way to get your typical, secured fiat loan by collateralizing it with crypto that you’d otherwise be hodling––at an incredible interest rate too.

Nexo

Product: Like BlockFi, Nexo is one of the more traditional new cryptocurrency lending tools out there. It offers a line-of-credit in fiat currencies (supports 45+ fiat currencies!) that’s collateralized by a user’s cryptocurrency investments. It functions pretty much exactly how a line-of-credit would function, except it provides a mechanism for those hodling crypto to get a line-of-credit while investing their assets. Nexo similarly makes profit from the cryptocurrencies that users invest in the platform and from charging users for its line-of-credit product.

Market: Nexo’s one of the few line-of-credit solutions collateralized with cryptocurrency, so it has a huge market to tackle and offers a pretty niche solution. It’s not generally targeted towards Dapps or small financial amounts, but rather larger, more robust financial situations.

Rates & Collateralization: Nexo offers 6.5% return on cryptocurrencies that you invest into their platform, which is infinitely higher than you’d get out of your typical savings or checkings account. The interest rates provide a massive incentive for people to open a Nexo account and take line-of-credit through this platform rather than relying on high-friction, slow traditional solutions.

Decentralization: Because of its nature as a very traditional financial product, the infrastructure of Nexo is very centralized. They take custody in all user investments and use that to structure their line-of-credit offerings. One pro to this is that it provides Nexo with a ton of institutional-backing; everything is SEC-/big bank-backed and they offer $100 million in custodial insurance for every loan on the platform.

Liquidity: On the lending side, Nexo offers fairly low-liquidity because it needs to retain user assets for a significant amount of time to collateralize lines-of-credit and make sufficient profit. On the buyer side, Nexo is extremely high-liquidity out of its nature as a line-of-credit; its entire product is focused on providing highly-liquid funds in a fast manner.

Traction and Funding: Nexo’s also doing incredibly funding-wise; they’ve raised $52.5 million from Arrington XRP Capital and quite a few private European and Swiss blockchain companies (Nexo is Swiss, so it makes sense that they’re mainly funded by players there).

Biggest Value Add: Nexo creates a huge incentive for users to try out the line-of-credit collateralized by the crypto model. Its interest rates are no joke, and it provides a very easy way for users to earn value out of their cryptocurrency that they’re probably just hodling around.

Maker

Product: Maker saw that much of the cryptocurrency lending market (and cryptocurrency market, in general) was highly dependent on the prices of the various coins, which makes it very volatile and reduces investor confidence. Maker sought to create a lending solution that balances out some of this volatility, and naturally, they made a stablecoin. They’ve launched a stablecoin called Dai (where 1 Dai = 1 USD) that they lend out, collateralized by other forms of cryptocurrency. They hope to increase customer confidence in crypto lending by adding some stability with a stablecoin model. Maker makes a stable profit by taking a small margin of the money it makes from loans before repaying it to the investing side.

Market: Much of Maker’s promotion is targeted towards smaller businesses that are interested in the cryptocurrency space, but see the volatility of the market as a bottleneck. Maker offers a very traditional lending model, where users can invest crypto and lend it out as usual, but the stablecoin makes it much less price-dependent and creates user confidence with such a volatile market.

Rates & Collateralization: Maker’s rates are always changing on the investing side, because they change the interest based on the volatile prices of the cryptocurrencies that users invest. All loans are collateralized up to 1.5x though, which helps add more security on top of the stablecoin element. The collateralization is structured a little differently with the stablecoin, because Maker has another coin called MKR. Holders of MKR can determine when the rates between Dai and other cryptocurrencies falls below a critical rate, and when collateralization needs to be redetermined and restructured. In essence, this allows MKR to have a board of crypto experts who know when the prices are getting too volatile and know how to restructure collateralization to maintain financial security.

Decentralization: It’s very decentralized. Everything is algorithmically balanced and determined and the company takes little-to-no custody in user assets.

Liquidity: Like most decentralized lending protocols, Maker offers a lot of liquidity. Borrowers and lenders can withdraw and deposit funds with fairly little friction––it’s a very simple process that’s made easier by the additional stability granted by the stablecoin.

Traction and Funding: Maker’s gotten a very positive response from the cryptocurrency venture community; most notably, Andreesen Horowitz recently invested $15 million into the platform and acquired 6% of the Maker token supply. On the customer side, MKR isn’t doing too shabby either; Dai has reached a total market cap around $55 million, which means it’s fairly active as a lending and trading tool.

Biggest Value Add: Maker helps create some confidence in the cryptocurrency lending community with its stablecoin model; ultimately, its biggest value is that it offers a lot more stability in a market that’s too often criticized for its volatility and incessant dependence on token prices.

Nuo

Product: Nuo functions very similarly to Maker––it offers a cryptocurrency lending protocol as you would prototypically think of it, where users invest one currency and can borrow in another. It’s not focused towards Dapps, so it literally is lending in its most basic form. In contrast to Maker, Nuo isn’t specifically focused on stablecoins and reducing volatility. Though Nuo offers Dai as one of its lending and borrowing options, they have a ton of other more traditional options that will appeal to the veteran crypto user. Nuo takes a small margin of the money it makes from loans to make its profit.

Market: Nuo captures a pretty generic market––essentially anyone who’s either looking to do something with cryptocurrency they’re just hodling, or anyone who’s looking to borrow a specific form of a cryptocurrency. Nuo supports fairly large loans too, so it’s more geared towards users than Dapps.

Rates & Collateralization: On the lender side, Nuo offers competitive 2-14% interest rates, depending on the type of cryptocurrency that users put into the platform. All loans are collateralized 1.5x the loan value, which is the standard for the cryptocurrency lending market.

Decentralization: Like most algorithmic lending tools, Nuo is also fairly decentralized. They take no custody in user assets and rely on their insanely powerful lending protocol to ensure that everything runs smoothly, but maintains the decentralization that blockchain enthusiasts know and love.

Liquidity: Similarly, Nuo’s algorithmic protocol lends it a very high liquidity where borrowers can request funds and lenders can withdraw or deposit their assets with little to no friction.

Traction and Funding: Nuo’s raised $250,000 from big Asian cryptocurrency investors like Amrish Rau and Jitendra Gupta; it’s also backed by ConsenSys and a few other sizable blockchain companies. It’s recently crossed $2 million in reserves in Asia, which makes it the largest lending protocol in the continent.

Biggest Value Add: Nuo offers a very versatile cryptocurrency tool that allows individuals to lend and borrow various forms of cryptocurrency quickly, efficiently, and securely. It also helps democratize the cryptocurrency lending market to Asia.

On Regulations and Licensing

Being a relatively new “currency” (or “commodity,” depending on who you ask), there’s always a huge debate on how products like these are regulated and licensed, and how they should be regulated. Much of the conversation on regulation centers around the treatment of smart contracts, which is the underlying technical mechanism for a lot of these products.

Smart contracts are generally regulated on a state-by-state basis, but the biggest regulations are imposed by the Commodities Futures Trading Commissions (CFTC). The CFTC essentially treats smart contracts like any other financial contract, which means it’s susceptible to all of the laws applicable to traditional financial models (like insurance, interest-rate regulated, etc.)

Final Thoughts

The cryptocurrency lending market is incredibly big, but has a lot of potential for financial growth. Compound, Dharma, BlockFi, Nexo, Maker, and Nuo all present extremely powerful products in the lending space that span a variety of use cases––from small margin loans for Dapps to entire line-of-credit solutions that bridge the gap between fiat and electronic trading. Altogether, the market has huge promise for innovation and profit––restructuring the way that we interact with cryptocurrency, fiat, and the intersection of them.

Digests

2019 Crypto Hegde Fund Report

This report provides an overview of the global crypto hedge fund landscape and offers insights into quantitative elements such as liquidity terms and performance, as well as qualitative aspects such as best practice with respect to custody and governance.

FinCEN’s new cryptocurrency guidance matches Coin Center recommendations | Coin Center

Multi-sig wallets, decentralized exchanges, and privacy protecting cryptocurrency developers are not regulated

Why should I rebuild a new TRON? – Network Volume – Medium

In the book The Left Hand of Darkness, Ursula K. Le Guin used the character Istravan to say something that I will never forget, “There is only one genius of me. That is, to know when to move that…

In the Tweets

Today in Congress Rep. Sherman called for a bill to ban all cryptocurrencies.

This is why Coin Center is needed in DC now more than ever. https://t.co/jgikm7z8bI

12:48 PM - 9 May 2019

16/ Heh okay FinCEN didn't say anything at all about lightning nodes. Nor are they going to. It's just silly. Honestly, people, stop with this stuff.

10:40 AM - 9 May 2019

News

Binance Security Breach Update – Binance

We have discovered a large scale security breach today, May 7, 2019 at 17:15:24 (UTC). Hackers were able to obtain a large number of user…

Bitstamp Hires Ex-Coinbase Trading Head to Court Wall Street Money - CoinDesk

Bitstamp, one of the longest-running cryptocurrency exchanges, has hired a former Coinbase executive and Wall Street veteran as its new head of U.S. operations.

Regulations

A Landmark for the Blockchain Island | Cointelegraph

Latest news from the “Blockchain Island” — a view from the Maltese Junior Minister for Financial Services, Digital Economy and Innovation.

Bitcoin Futures & Custody: Bakkt’s differentiated approach

I n our recent post, Bakkt COO Adam White laid out our custody roadmap and how secure digital asset storage is central to our strategy. Today, we’re pleased to update you on the launch of bitcoin…

New Products and Hot Deals

Ex-SoFI CEO's Startup Closes $1 Billion Credit Line on a Blockchain - CoinDesk

Figure Technologies, a fintech startup founded by former SoFi CEO Mike Cagney, has closed a $1 billion “uncommitted” line of credit on a blockchain.

Crypto Wallet Abra Adds In-App Support for 'Thousands' of US Banks - CoinDesk

Cryptocurrency wallet and investment app Abra now allows users to connect accounts from “thousands” of U.S. banks, the firm announced Thursday.

bloXroute raises $10M to date to solve the blockchain scalability bottleneck

We are excited to announce the closing of our Simple Agreement for Future Tokens (SAFT) with participation from Pantera, Coinbase Ventures, Fenbushi, and others. bloXroute was founded by blockchain…

Additional Info

Results from last week's poll are shown above

👋 Working on building new technologies? I’d love to hear about it, shoot me an email

🙏 I’d appreciate it if you forwarded this email to someone who would might benefit from it

💡If you have any content you want to share on this newsletter, please send it to me and we can make it happen

Please click here to help me improve this newsletter and your experience by answering ONE question!

Meet with Me

New York, Token Summit, May 16

Las Vegas, July 12